Europe is less prepared for geopolitical shift

The early weeks of the second term of office of US President Donald Trump had led to a significant upheaval in the European Union. Now it seems, starting from the second quarter, the US will use reciprocity as a justification for increasing import tariffs on European goods in sectors where European tariffs are higher than those in the US. Trump’s administration also views VAT as an additional import rate in Europe, which can increase the scope for rising US tariffs.

Simultaneously, Trump has advocated a ceasefire in Ukraine, mostly putting aside Europe and Ukraine as a potential partner in negotiations. While peace in Ukraine will be beneficial for the business and consumer sentiment and has the potential to reduce energy prices, the agreement has not been guaranteed – especially if Russia is treated too profitable. Meanwhile, the US has explained that Europe must increase its own defense efforts, because the US is less willing to continue to guarantee European security. This has caused confusion and anger in the European capital, but there is no clear general response that appears so far.

More defense expenditure

In a positive note, the German election only produces one proper coalition: “large coalition” between CDU/CSU and SPD. Unfortunately, scrambling with the two -thirds of the majority needed to change the debt brake seems to be challenging. However, we remain convinced that the new Chancellor, Friedrich Merz, will find a way – such as declaring a fiscal emergency – to increase government spending, especially for defense. Germany still has some budget space for fiscal expansion.

Other countries that also need to increase defense expenditure (Europe may have to move from about 2% to 3.5% from GDP over the next five years), but have fewer fiscal spaces, need to find savings elsewhere. In addition, when considering the long delay and high import content of military expenditure, GDP stimulus for this year and next year seems limited. Nevertheless, we have added 0.1 percentage points to the estimated growth of our 2026, and encouragement for 2027 can be slightly higher. The possibility of additional military expenditure financed by European defense funds with a small loan capacity is small for now.

Source: LSEG DATASTREAM, ING

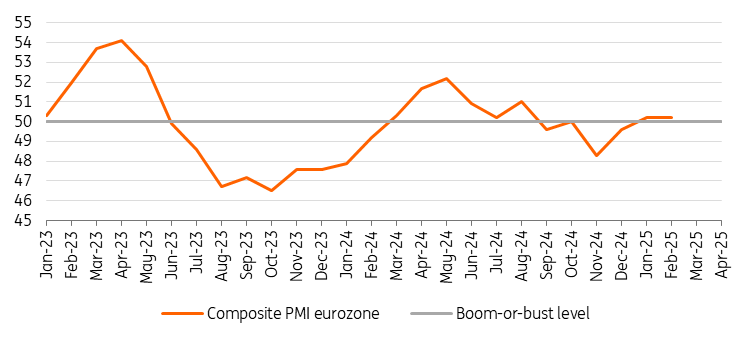

The economic situation is not as bad as the feared market

Since December, European economic indicators have shocked positively, mainly because they are not as bad as the market expected. The best description for the economic situation of the Euro zone seems to be “bottoming out.” The combined PMI is stable at 50.2 in February, right above the boom-or-bust level. However, the new order component remains weak and the job falls, especially in the field of manufacturing. Disappointing consumption due to less positive assessment of the labor market, which leads to a higher level of savings. Although there is a potential for stronger consumption growth, geopolitical uncertainty does not help increase consumer confidence. Therefore we maintain our growth estimates by 0.7% for this year, while raising it to 1.3% for 2026, driven by additional military expenditure.

ECB approaches the neutral level

Inflation tends to remain above the projection of the European central bank in the first quarter, and higher input prices in both manufacturing and services have increased the expectations of selling prices. At the same time, the ECB wage tracking continues to show a slowdown in wage growth in the second half. In February, the ECB issued an estimated neutral interest rate, which ranged from 1.75% and 2.25% based on the latest model updates, and between 1.75% and 3.0% based on all available models.

Therefore it is not surprising that ECB Director Isabel Schnabel stated that the central bank approaches the point where he might need to pause or stop the interest of interest rates. We still believe that 2% will be achieved in the summer, and 1.75% is feasible if the increase remains very calm. However, the consensus in the central bank seems to be that any recovery may quickly face supply constraints, making it a risk to adopt a monetary policy that is too expanded.

Source: Ing, https://think.ing.com/articles/eurozone-geopolitics-the- fore-eurozone/?utm_campaign=february-27_eurozone-geopolitics-to-the-eurozone&utm_mediu